When most beginners think about financial markets, they usually think about the stock market first. Stocks are popular, easy to hear about in the news, and often connected to famous companies like Apple, Microsoft, Tesla, or Amazon.

But behind the scenes, there is another market that plays a huge role in the global economy: the bond market.

The bond market may not sound as exciting as stocks, crypto, or forex, but it is one of the most important financial markets in the world. Governments use it to finance public projects. Companies use it to raise money for expansion. Banks, pension funds, insurance companies, and investors use it to generate income and manage risk.

For beginners, bonds can seem confusing at first because they are different from stocks. When you buy a stock, you own a small part of a company. When you buy a bond, you are usually lending money to a government, company, or organization.

In this guide, we will explain what the bond market is, how bonds work, why bond prices move, how investors make money from bonds, and what risks you should understand before investing.

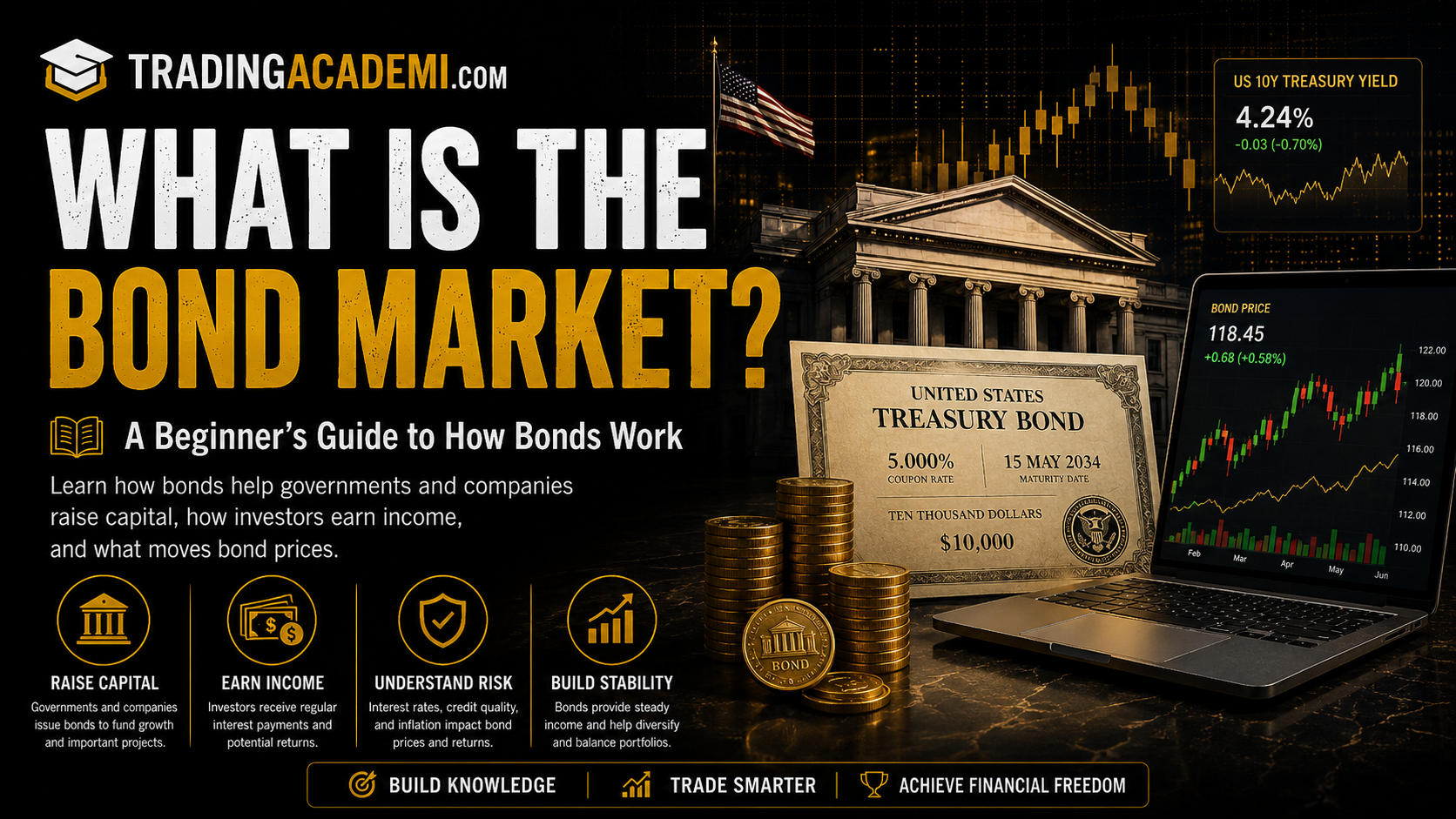

What Is the Bond Market?

The bond market is a financial market where investors buy and sell debt securities called bonds.

A bond is basically a loan.

When an investor buys a bond, they are lending money to the bond issuer. The issuer can be a government, a corporation, a municipality, or another organization. In return, the issuer usually agrees to pay interest over time and repay the original amount when the bond reaches its maturity date.

This is why the bond market is also called the debt market or fixed-income market.

The word “fixed income” comes from the fact that many bonds pay a fixed interest amount to investors. However, not all bonds work exactly the same way. Some have fixed rates, some have variable rates, and some are linked to inflation or other financial conditions.

The basic idea remains simple:

A borrower needs money.

An investor lends money by buying a bond.

The borrower pays interest.

The investor receives income and later gets the principal back if everything goes as planned.

Why Does the Bond Market Exist?

The bond market exists because governments and companies often need to raise large amounts of money.

Instead of borrowing from only one bank, they can issue bonds to many investors. This allows them to collect capital from the market.

For example, a government may issue bonds to finance roads, schools, hospitals, military spending, or public services. A company may issue bonds to build factories, launch new products, refinance old debt, or expand into new markets.

At the same time, investors buy bonds because they may want regular income, portfolio stability, or lower risk compared to certain stocks.

This creates a connection between borrowers and investors.

The bond market helps money move from people and institutions that have capital to those who need capital.

How Does a Bond Work?

To understand bonds, imagine that a company wants to borrow money.

Instead of asking one bank for the full amount, the company issues bonds. Each bond represents a small piece of that loan.

When you buy one of those bonds, you are lending money to the company.

A typical bond has several important parts:

Face value

This is the amount the bond issuer agrees to repay at maturity. Many bonds have a face value of $1,000, but this can vary.

Coupon rate

This is the interest rate the bond pays. For example, if a bond has a 5% coupon rate and a $1,000 face value, it may pay $50 per year in interest.

Maturity date

This is the date when the issuer must repay the face value to the investor.

Issuer

This is the government, company, or organization borrowing the money.

Market price

This is the price at which the bond trades in the market. It can be higher or lower than the face value.

Simple Bond Example

Let’s say you buy a corporate bond with these conditions:

Face value: $1,000

Coupon rate: 5%

Maturity: 10 years

This means the company promises to pay you $50 per year in interest. After 10 years, the company repays the $1,000 principal, assuming it does not default.

So, if everything goes well, you receive interest income every year and get your original investment back at the end.

This is why many investors use bonds for income and stability.

However, bonds are not risk-free. The issuer may face financial problems, interest rates may change, and the bond price may move before maturity.

Bond Market vs Stock Market

The bond market and stock market are both important, but they work differently.

When you buy a stock, you become a partial owner of a company. Your profit depends on the stock price rising, dividends, or both.

When you buy a bond, you are lending money. Your return usually comes from interest payments and repayment of principal.

Stocks can offer higher growth potential, but they are often more volatile. Bonds are usually considered more stable, but their returns may be lower.

Here is a simple comparison:

| Feature | Bond Market | Stock Market |

|---|---|---|

| What you buy | Debt | Ownership |

| Investor role | Lender | Shareholder |

| Main return | Interest payments | Price growth and dividends |

| Risk level | Often lower, but not risk-free | Often higher |

| Priority if company fails | Bondholders usually rank before shareholders | Shareholders are usually last |

| Best known for | Income and stability | Growth and ownership |

This does not mean bonds are always safe or stocks are always risky. It depends on the issuer, market conditions, interest rates, and the investor’s strategy.

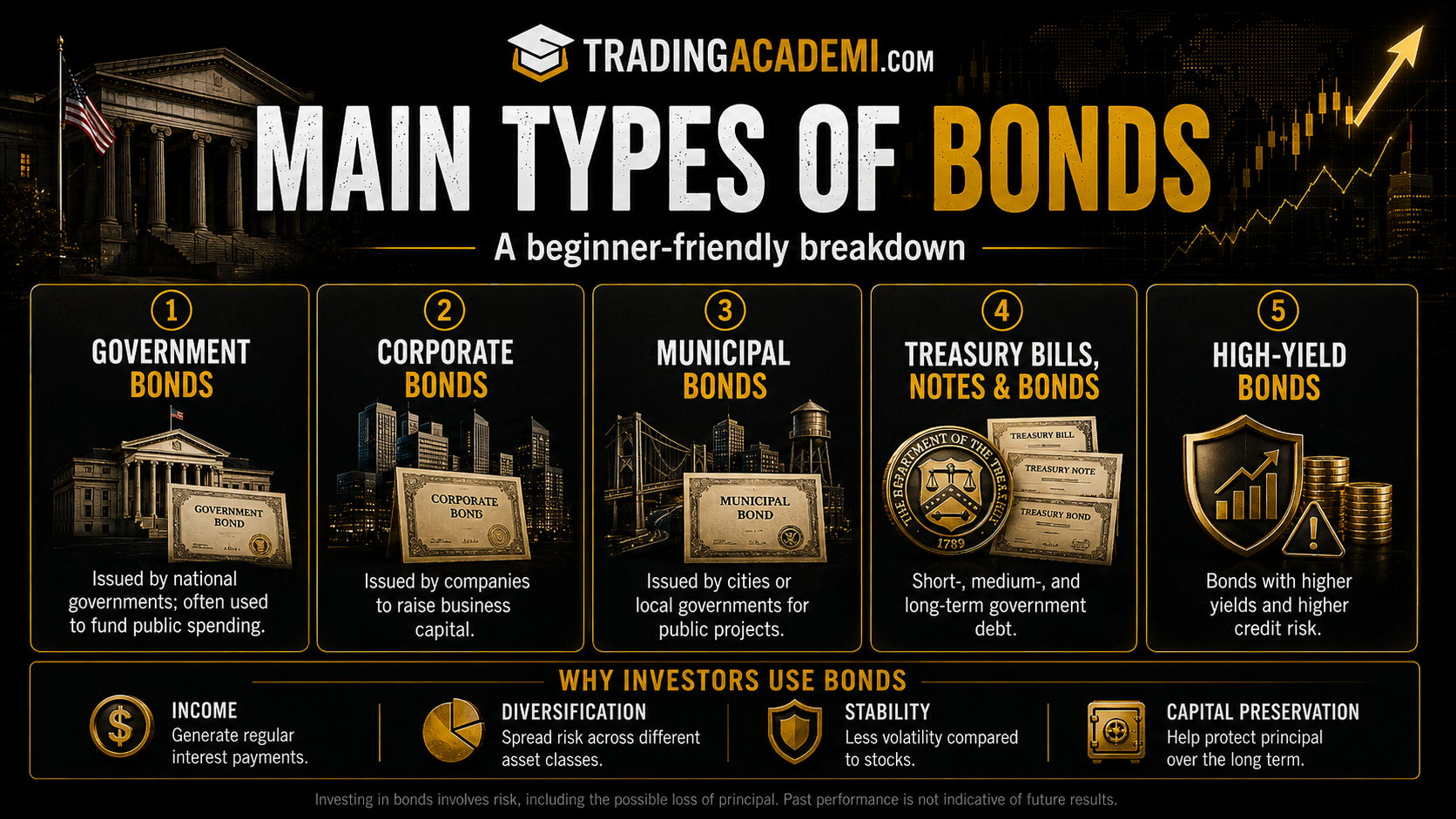

Main Types of Bonds

There are many types of bonds, but beginners should start with the most common categories.

1. Government Bonds

Government bonds are issued by national governments to raise money.

For example, the U.S. government issues Treasury bonds, Treasury notes, and Treasury bills. Other countries also issue government bonds in their own currencies.

Government bonds from stable countries are often considered lower risk because the government has the ability to collect taxes and manage monetary policy. However, government bonds can still be affected by inflation, interest rates, currency risk, and political or economic instability.

2. Corporate Bonds

Corporate bonds are issued by companies.

A company may issue bonds to finance expansion, buy equipment, refinance debt, or support business operations.

Corporate bonds usually pay higher interest than government bonds because companies generally carry more risk than stable governments.

A strong company with good financial health may issue bonds at a lower interest rate. A weaker company may need to offer a higher rate to attract investors.

3. Municipal Bonds

Municipal bonds are issued by cities, states, or local governments.

They are often used to finance public projects such as schools, roads, bridges, water systems, or hospitals.

In some countries, municipal bonds may offer tax advantages, depending on local laws and the investor’s situation.

4. Treasury Bills, Notes, and Bonds

These are different types of government debt based mainly on maturity.

Treasury bills are short-term debt instruments.

Treasury notes are medium-term debt instruments.

Treasury bonds are long-term debt instruments.

They are commonly used by investors who want exposure to government debt.

5. High-Yield Bonds

High-yield bonds are bonds issued by companies or entities with lower credit ratings.

They are also sometimes called “junk bonds.”

These bonds usually pay higher interest because they carry higher risk. The issuer may have a greater chance of defaulting compared to a financially strong borrower.

High-yield bonds can be attractive because of their income potential, but beginners should be careful because higher yield usually comes with higher risk.

What Is Bond Yield?

Bond yield is one of the most important concepts in the bond market.

Yield measures the return an investor can expect from a bond.

Many beginners confuse coupon rate and yield. They are related, but they are not always the same.

The coupon rate is the interest rate based on the bond’s face value.

The yield depends on the price you pay for the bond and the income it generates.

For example, if a bond pays $50 per year and you buy it for $1,000, the yield is 5%.

But if the bond price drops to $900 and it still pays $50 per year, the yield becomes higher because you are earning the same income on a lower purchase price.

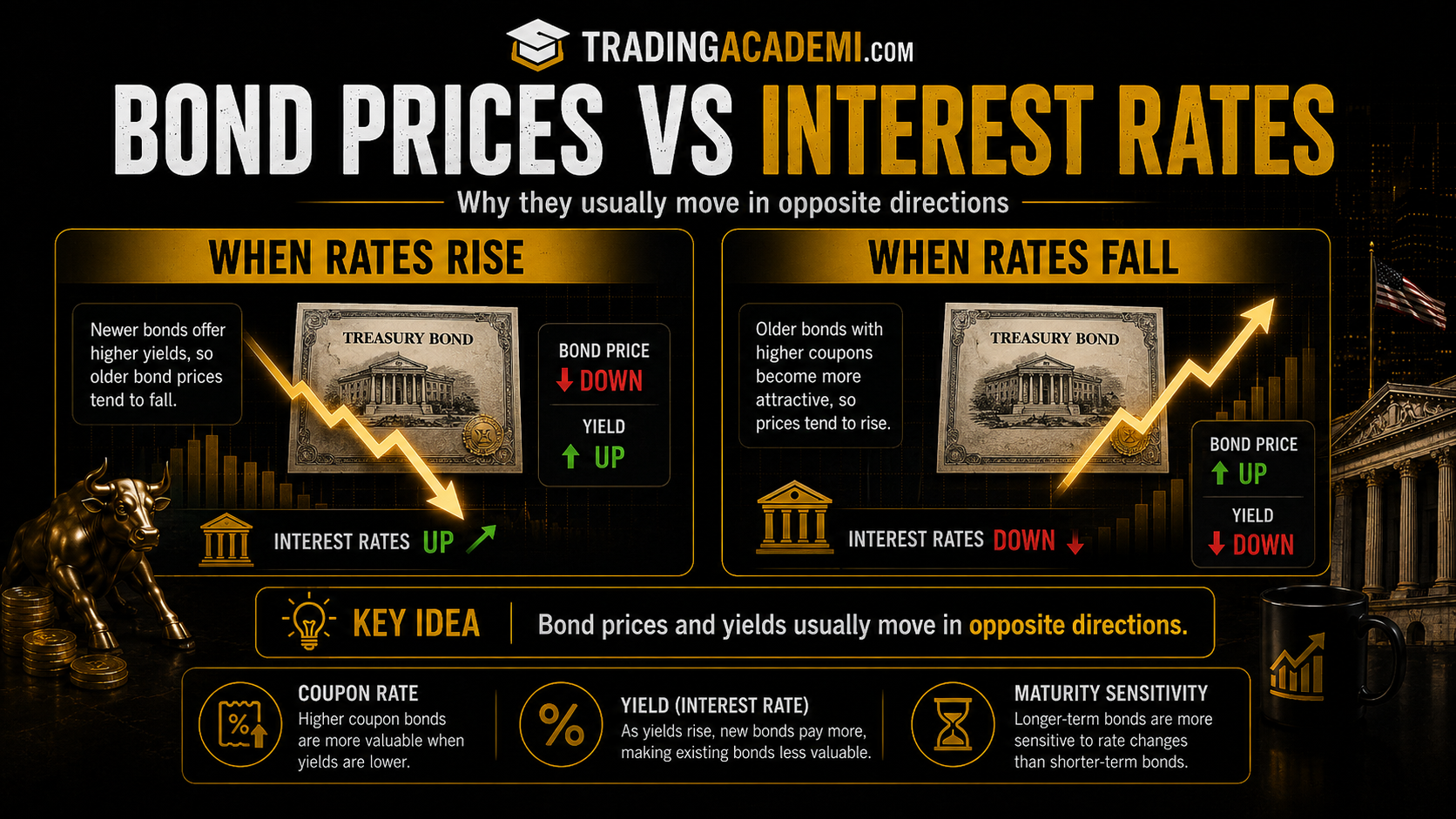

This is why bond prices and yields move in opposite directions.

Why Bond Prices and Interest Rates Move Opposite

One of the most important rules in the bond market is this:

When interest rates rise, bond prices usually fall.

When interest rates fall, bond prices usually rise.

Here is why.

Imagine you own a bond that pays 3% interest. Later, new bonds are issued paying 5%. Investors will prefer the new bonds because they offer higher income.

To make your older 3% bond attractive, its market price may need to fall.

Now imagine the opposite. You own a bond paying 5%, but new bonds are only paying 3%. Your bond becomes more attractive, so its market price may rise.

This relationship between rates and bond prices is one of the key reasons the bond market reacts strongly to central bank decisions, inflation data, and economic expectations.

What Makes Bond Prices Move?

Bond prices can move for several reasons.

Interest Rates

Interest rates are one of the biggest drivers of bond prices. When central banks raise or lower rates, bond markets often react quickly.

Inflation

Inflation reduces the purchasing power of future payments. If inflation rises, investors may demand higher yields to compensate for the loss of purchasing power.

Credit Risk

If investors believe a company or government may struggle to repay its debt, the bond price may fall and the yield may rise.

Economic Growth

A strong economy can push interest rates higher if inflation becomes a concern. A weak economy can increase demand for safer bonds.

Market Sentiment

During uncertain periods, investors may move money into safer bonds. During risk-on periods, they may prefer stocks or higher-yielding assets.

Time to Maturity

Long-term bonds are usually more sensitive to interest rate changes than short-term bonds.

Who Uses the Bond Market?

The bond market is used by many participants.

Governments issue bonds to finance public spending.

Corporations issue bonds to raise business capital.

Banks and institutions trade bonds for income, liquidity, and risk management.

Pension funds use bonds to match long-term obligations.

Insurance companies use bonds to support future claims.

Individual investors may use bonds for income and portfolio diversification.

The bond market is not only for professional traders. Many retail investors access bonds through bond funds, ETFs, or retirement accounts.

How Investors Make Money From Bonds

Investors can make money from bonds mainly in three ways.

1. Interest Income

This is the most common reason investors buy bonds.

If a bond pays regular interest, investors can receive income over time.

2. Price Appreciation

If a bond’s market price rises, an investor may sell it for more than they paid.

This can happen when interest rates fall or when the issuer’s credit quality improves.

3. Holding to Maturity

Some investors buy bonds and hold them until maturity. If the issuer does not default, they receive interest payments and get the principal back at maturity.

This strategy may reduce the impact of short-term price changes, but it does not remove all risks.

Are Bonds Safe?

Bonds are often considered safer than stocks, but that does not mean they are risk-free.

A government bond from a stable country is usually considered lower risk than a bond issued by a weak company. But every bond has some type of risk.

The main risks include:

Interest rate risk

Inflation risk

Credit risk

Default risk

Liquidity risk

Reinvestment risk

Currency risk

Beginners should never assume that a bond is safe only because it is called a bond. The quality of the issuer matters.

Bond Ratings Explained

Bond ratings help investors understand the credit quality of a bond issuer.

Credit rating agencies evaluate the ability of governments and companies to repay their debt.

Higher-rated bonds are usually considered safer but pay lower yields. Lower-rated bonds usually pay higher yields but carry more default risk.

Investment-grade bonds are generally considered higher quality. High-yield bonds are considered riskier.

For beginners, bond ratings are useful, but they should not be the only factor in the decision. Ratings can change, and markets sometimes react before ratings are updated.

What Is Default Risk?

Default risk is the risk that the bond issuer fails to make interest payments or repay the principal.

If a company issues bonds and later faces serious financial problems, it may default on its debt.

When default risk rises, investors usually demand higher yields. This means the bond price may fall.

Government bonds from strong economies usually have lower default risk, while corporate bonds from weaker companies may have higher default risk.

What Is Duration?

Duration is a measure of how sensitive a bond is to interest rate changes.

A bond with a longer duration usually moves more when interest rates change. A bond with a shorter duration usually moves less.

For example, a long-term bond may fall more sharply when interest rates rise compared to a short-term bond.

This is important because some beginners think bonds cannot lose value. But if interest rates rise quickly, long-term bonds can experience significant price declines.

Bond Funds and Bond ETFs

Many beginners do not buy individual bonds directly. Instead, they use bond funds or bond ETFs.

A bond fund holds a group of bonds. This can provide diversification because the investor is not relying on only one bond issuer.

Bond ETFs trade on exchanges like stocks, making them easier to buy and sell.

However, bond funds and ETFs do not always behave exactly like individual bonds held to maturity. Their prices can move daily based on interest rates, credit conditions, and market demand.

Bond funds can be useful, but investors should understand what type of bonds the fund holds.

Why Investors Add Bonds to a Portfolio

Investors often use bonds for several reasons.

Income

Bonds can provide regular interest payments.

Diversification

Bonds may help balance a portfolio that also contains stocks.

Stability

High-quality bonds may be less volatile than stocks during certain market conditions.

Capital Preservation

Some investors use bonds to reduce risk and preserve capital, especially as they get closer to important financial goals.

Risk Management

Institutions use bonds to manage liabilities, cash flow, and interest rate exposure.

Bonds are not only about making money. They are also about managing risk.

Common Beginner Mistakes With Bonds

One mistake is thinking all bonds are safe.

Another mistake is chasing the highest yield without understanding why the yield is high. A high yield can be a warning sign that the issuer is risky.

Some beginners also ignore interest rate risk. They buy long-term bonds without realizing that rising rates can reduce the bond’s market value.

Another mistake is not understanding the difference between individual bonds and bond funds.

Finally, some investors buy bonds without checking the issuer’s credit quality, maturity date, yield, and fees.

Bond Market vs Money Market

The bond market and money market are related, but they are not the same.

The money market focuses on short-term borrowing and lending, usually with instruments that mature in one year or less.

The bond market includes medium-term and long-term debt securities.

Money market instruments are often used for short-term liquidity. Bonds are often used for income, financing, and longer-term investment strategies.

Recommended reading:

What Is the Money Market?

Bond Market vs Stock Market: Which Is Better?

There is no simple answer.

Stocks may offer higher long-term growth potential, but they usually come with higher volatility.

Bonds may offer more stable income, but they can still lose value and may offer lower returns.

The better choice depends on your goals, risk tolerance, time horizon, and market conditions.

Many investors use both stocks and bonds together instead of choosing only one. This helps create a more balanced portfolio.

Recommended reading:

What Is the Stock Market?

How to Start Learning the Bond Market

A beginner should start by understanding the basic vocabulary:

Bond

Issuer

Coupon

Yield

Maturity

Face value

Credit rating

Default risk

Duration

Interest rate risk

After learning these terms, it becomes easier to understand why bonds move and how they fit into a portfolio.

You do not need to become a professional bond trader to understand the basics. But you should know enough to avoid common mistakes.

Final Thoughts

The bond market is one of the most important parts of the financial system. It allows governments and companies to raise money, and it gives investors a way to earn income and manage risk.

Bonds may look simple, but they are influenced by interest rates, inflation, credit quality, maturity, and market sentiment.

For beginners, the key is to understand that bonds are loans, not ownership. When you buy a bond, you are lending money and expecting interest payments plus repayment of principal.

A smart investor does not buy bonds only because they seem safe or because the yield looks attractive. A smart investor looks at the issuer, the maturity, the yield, the risks, and how the bond fits into the overall strategy.

The bond market may be less popular than stocks, but understanding it can make you a much stronger and more informed market participant.

Educational Disclaimer

This article is for educational purposes only and should not be considered financial advice. Investing and trading involve risk, including the possible loss of capital. Always do your own research or consult a qualified financial professional before making financial decisions.